PAGE 01 · Front cover

A MORE Group Field Manual

2026 EDITION

Buy

Phuket

Right

The Insider Framework for Smart Property Investment in Thailand's Top Resort Market

Buy Phuket Right — The Insider Framework for Smart Property Investment in 2026

First edition published 2026 by MORE Group, Phuket, Thailand.

© 2026 MORE Group. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and articles.

For permissions, partnership and press inquiries write to hello@moregroup.estate.

Notice & disclaimers

This book is orientation, not advice. It is intended to give an international buyer a working framework for understanding the Phuket property market. It is published by MORE Group as an educational reference.

By continuing to read, the reader acknowledges and accepts the framing above.

Cover and interior design: MORE Group Studio.

Set in Fraunces, Inter and JetBrains Mono.

Printed-quality PDF. Online edition available at book.moregroup.estate.

Phuket is sold. By developers, sales offices, influencers with affiliate links, glossy magazines flying the editor in for a weekend. Most of what reaches a foreign buyer is marketing dressed as analysis — a press release with a yield number attached.

This book is the opposite of that. After eight years running deals on this island, we kept watching the same conversation repeat. A buyer would arrive with brochures promising 8–12% guaranteed returns; we’d spend the first two meetings unwinding numbers that didn’t survive contact with a tax adviser. The brochure had won the attention war. The buyer had already made an emotional commitment to the wrong unit. We wrote this book to win those two meetings back — and to give them to readers who will never sit across from us.

What you’re reading is the framework we use internally to underwrite a deal. The same scoring methodology, the same risk patterns, the same district numbers. We removed the names of bad projects (Thai law makes that the right call) and kept the patterns. Every claim is one our team would defend in a Knight Frank meeting.

It’s also unfinished. Markets shift, the 2027 edition will have new data, and if you find a number you can falsify — write to us. Phuket is one of the most interesting residential markets in Asia, and one of the most expensive places to learn lessons in. This book tries to make those lessons cheaper.

— The MORE Group team · Phuket, Q2 2026

Three buyer profiles use Phuket for three different things. We wrote this book so each profile can find their thread without reading 125 pages cover-to-cover. Read the part that fits you, skim the part that doesn’t, return to the appendices when you need them.

You hold property in 2+ jurisdictions. Phuket is a defensive position — quality, branded, hold for 10+ years.

Read in this order: Ch 1, 3, 6, 10–11, 18, 20, 25, 27.

Skim: Ch 12, 22.

You’re moving here, partially or fully. The asset is a home first, an investment second. Family, schools, community matter.

Read in this order: Ch 1, 5, 7, 13–14, 17, 19, 24.

Skim: Ch 3, 22, 23.

You’re here for cash flow. Hotel-managed, condotel, exit in 5–7 years when the cycle turns.

Read in this order: Ch 2, 4, 6, 12, 15, 17, 22–23, 25–26.

Skim: Ch 13, 19.

One. Read the Reservation Agreement appendix (C) first. It’s the document you’ll sign before anything else; understanding it changes how you read the rest. Two. Bookmark the Red Flags Index (E). You’ll come back to it. Three. Keep Appendix G · Sources open in a separate tab — every claim in this book traces to it.

A note on time. Read this book over 5‑6 sittings, not in one go. The framework is designed to be argued with — mark it up, write in the margins, send us your disagreements. The next edition will be better because of them.

Phuket has quietly outgrown its postcard image. The island is still the Andaman’s most photographed coastline, but in the last five years it has also become Southeast Asia’s most institutional resort-property market outside Singapore. Three forces explain the shift.

Roughly 88 branded residences are now operational or under construction across the island, anchored by Banyan Tree, Anantara, MGallery, Marriott, Hilton, Hyatt and Wyndham. Branded inventory underwrites resale liquidity in a way no independent project can match.

International arrivals returned to 12.5M in 2025 versus 9.9M in 2019. More importantly, the new Long-Term Resident visa (10-year) is producing a measurable layer of stay-longer-than-90-days demand that did not exist in the previous cycle.

Through the 2024–2026 cycle, the Thai Baht has been one of the steadier major Asian currencies against the US Dollar. For a portfolio carrying euro or sterling exposure, that stability is itself a position — quietly, without the volatility of Dubai dirham pegs or Indonesian rupiah swings.

Before any spreadsheet, ask: would this property still be desirable if rental income were zero? If yes, you are buying a real asset. If no, you are buying a yield assumption.

What changed Phuket structurally was the moment hotel groups started signing residential components on terms that survive a downturn. The pipeline below covers projects operational, under construction, or with planning consent secured by Q1 2026.

| Operator family | Operating | Under build | Total 2027F |

|---|---|---|---|

| Marriott family (JW, Autograph, Westin) | 9 | 7 | 16 |

| Accor family (MGallery, Sofitel, Banyan Tree) | 11 | 6 | 17 |

| Hilton & Hyatt | 5 | 4 | 9 |

| Anantara & Minor Hotels | 7 | 3 | 10 |

| Wyndham, Best Western, Centara | 12 | 5 | 17 |

| Independent & boutique brands | 14 | 5 | 19 |

| All branded residences | 58 | 30 | 88 |

Source: MORE Group pipeline tracker, Q1 2026; cross-referenced with operator releases, Land Office permits, STR Global hotel data. Excludes single-villa projects below 12 units.

Five operator families control 78% of forthcoming inventory (69 of 88 projects) — the resale audience behaves institutional, not holiday-home.

Most prospectuses you will read about Phuket lead with yield. That is a conversation about an income stream. The conversation worth having first is about the currency that income stream is denominated in.

The Thai Baht has held within a 3.5% band against the US Dollar across the 2024–2026 cycle — tighter than the Indonesian rupiah, the Vietnamese dong, the Malaysian ringgit, and far tighter than either sterling or the euro through the same window. For a portfolio that earns in GBP or EUR and stores wealth in USD, owning a Thai-baht-denominated asset behaves like a defensive overlay.

Institutional supply, year-round demand, defensive currency. The next chapter puts numbers on all three.

A snapshot of new-build asking prices, reset to USD per square metre. Numbers are medians of MORE Group’s tracked inventory, not promotional ranges.

| District | Condo USD/m² | Villa USD/m² | Indicative yield |

|---|---|---|---|

| Bang Tao & Layan | 5,400 | 4,900 | 6.0‑7.5% |

| Laguna | 5,800 | 5,200 | 5.5‑6.5% |

| Surin & Kamala | 6,800 | 7,400 | 5.5‑6.8% |

| Patong | 3,900 | 3,200 | 7.0‑9.0% |

| Rawai & Nai Harn | 3,400 | 3,000 | 5.0‑6.0% |

| Cherngtalay & Thalang | 2,900 | 2,500 | 5.0‑6.5% |

| Mai Khao & Nai Yang | 4,200 | 3,800 | 6.2‑7.8% |

| Phuket Town | 2,900 | 2,400 | 5.5‑6.5% |

| Phuket median | 4,050 | 3,500 | 6.0% |

Source: MORE Group internal price book, Q2 2026, n = 299 active projects. Yields reflect long-let scenarios with conservative 70% occupancy, net of management fees. Asking prices currently transact 3–12% below first listing depending on segment and stage of pre-launch discounting.

Three rental modes dominate Phuket. The ranges below are net — after operator share, CAM and sinking fund, before home-country income tax.

| Rental mode | Gross | Net | Effort & risk profile |

|---|---|---|---|

| Long-let 12-month tenancy |

5.5‑7.0% | 4.5‑6.0% | Lowest variance, lowest active management. One tenant, one currency, one tax line. |

| Hotel-managed Branded operator pool |

7.5‑10.0% | 5.5‑7.5% | Operator takes 30–40%. FF&E reserves 3–5%. Exit penalties common — read clause 14. |

| Self-managed short-let Airbnb / direct |

9.0‑14.0% | 5.0‑8.5% | Highest theoretical return. Highest variance. Hotel Act exposure if condo strata permits short-let — many do not. |

The biggest line is operator share on hotel-managed pools (30–40%). Next is the cost stack — CAM, sinking fund, insurance, agency fee — absorbing 15–25% of gross. Short-let income then attracts 5–15% Thai withholding before home-country tax.

A clean 5% long-let often beats a notional 8% short-let. The right yield is the one whose effort and tax profile match yours.

Property markets in resort cities live on top of two layers: tourism flow (the demand for shelter) and the macro environment (the cost of capital). For Phuket, five indicators carry most of the signal. Track these five and you will know more about the market than most brochure-writers do.

| Indicator | 2019 | 2025 | 2026F | Signal |

|---|---|---|---|---|

| Phuket arrivals (M) | 9.9 | 12.5 | 13.2 | Short-let demand |

| Hotel ADR (USD, 5-star) | 285 | 410 | 425 | Short-let ceiling |

| BoT policy rate | 1.50% | 1.25% | 1.00% | Cost of THB capital |

| Thai GDP growth | 2.1% | 2.2% | 1.6% | Domestic demand |

| CPI (Thailand) | 0.7% | −0.1% | 0.3% | Real-yield input |

Sources: Tourism Authority of Thailand 2025 annual report; Bank of Thailand Monetary Policy Report, February 2026 (policy rate, GDP, CPI); STR Global Phuket hotel benchmarking. Macro forecasts are BoT central estimates; mid-point shown for ranges. Figures revised to reflect the BoT’s February 2026 policy round.

Two patterns deserve attention. Phuket tourism sits 26% above 2019 and ADR is 44% higher — the island is taking share within Thailand and pricing more confidently. At the same time, the cost of THB capital is the lowest it has been in over a decade, and headline inflation is in the dip-zone. Real yield on Phuket rental property has rarely looked wider against domestic alternatives.

No single market wins on every dimension. The matrix below benchmarks Phuket against the three destinations most commonly considered alongside it by offshore HNW buyers in 2026.

| Criterion | Phuket | Bali | Dubai | Cyprus |

|---|---|---|---|---|

| Foreign ownership | Freehold condo (49%) | Long lease only | Freehold in zones | Full freehold |

| Entry price, condo | $4,300 | $3,200 | $6,800 | $4,200 |

| Net yield range | 5.0‑7.5% | 6.0‑9.0% | 5.5‑7.0% | 3.5‑5.0% |

| 5-yr capital growth | +34% | +41% | +62% | +18% |

| Currency vs USD | THB band ~3.5% | IDR ~7% | AED pegged | Eurozone vol |

| Residency pathway | LTR 10-yr | KITAS | Golden Visa 10-yr | PR by investment |

| Days to sell, avg | 120‑180 | 180‑240 | 60‑120 | 150‑240 |

| Regulatory drift | Low | Medium | Low | EU-bound |

Sources: Knight Frank Wealth Report 2026 (capital growth); Savills World Cities Index 2026 (entry prices); Henley Passport Index 2026 (residency pathways); JLL Dubai market report; Colliers Indonesia Q4 2025; RICS Cyprus market view; IMF currency reports. MORE Group transaction data for Phuket. All metrics for Q1 2026.

Read the matrix on the previous page through the lens of the kind of buyer you are. The same numbers tell different stories.

Dubai wins on five-year growth, but with the highest entry price and a market that re-prices on news. The headline gain assumes you sold in a strong window. Phuket and Bali offer steadier mid-cycle growth on a lower base.

Bali tops the gross-yield league but on shorter, less protected lease structures and in a currency with double the volatility band. Phuket delivers the best risk-adjusted yield in the region for a hold period of 5+ years — particularly for hotel-managed inventory.

Cyprus exposes you to euro cycles. Dubai rides the dollar peg. Phuket sits in the cleanest middle ground — a managed-band currency that has outperformed its regional peers through three consecutive macro shocks (2020, 2022, 2024).

Cyprus still leads on EU-passport optionality, though that route narrows annually. Dubai’s Golden Visa is the cleanest 10-year pathway tied to a property purchase. Phuket’s LTR visa rewards passive income and works as a complement to, not a substitute for, your existing residency.

The case below is a composite drawn from MORE Group’s 2024–2025 advisory pipeline. Names and identifying details are changed; the decision logic is real. We use it because the elimination process is more useful than the conclusion.

A London-based fintech founder, 42, with a planned hold horizon of seven years and a budget of USD 1.2M for a single asset. Existing portfolio: London townhouse, NYC condo, two Lisbon flats. Currency exposure already heavy in GBP, EUR, USD.

James bought late 2024 at USD 5,200/m². Phuket won by adding what his portfolio lacked.

Each risk below is a pattern: an observable behaviour, not an accusation. We deliberately name no developers or buildings. Learn to recognise the pattern, not the project.

| # | Pattern | What to look for |

|---|---|---|

| 1 | Off-plan delivery slip | Two or more projects from the same developer with handover dates that have moved by more than nine months. |

| 2 | Foreign-quota saturation | A condo where the foreign-quota register is already 85%+ filled before launch ends. |

| 3 | Title-category mismatch | A “freehold” villa sitting on Nor Sor 3 Gor land rather than Chanote. Convertible, but not quickly. |

| 4 | CAM creep | Common-area fees set 25%+ below comparable buildings — subsidy at launch or under-engineering. |

| 5 | Yield guarantee above earning power | An 8%+ five-year guarantee on a building whose hotel benchmark earns 5–6%. The gap is paid by future buyers. |

| 6 | Currency-mismatched payments | SPA priced in THB, invoiced in USD at “developer’s rate”. Historical drift: 1.5–3% against the buyer. |

Sources: Bangkok Post real-estate desk (2018–2025), Thai Arbitration Institute case digests, Phuket Land Office gazette, Bank of Thailand FX manual.

| # | Pattern | What to look for |

|---|---|---|

| 7 | First-time developer | An SPV with no completed Thai project. The marketing brand may be new even when the parent is established — check the SPV signing your contract. |

| 8 | Single-bank escrow | Deposits routed through one branch of one bank with no segregated escrow. Concentration risk surfaced twice in adjacent ASEAN markets. |

| 9 | Setback drift | Beachfront renders showing structures inside the 30m setback line. Enforcement tightened twice since 2018. |

| 10 | Resale liquidity collapse | Micro-markets with 800+ units coming online in 24 months into the same buyer profile. Resale times have tripled. |

| 11 | Operator exit penalty | Hotel-management exit penalties of 12–36 months of pooled gross revenue. The contract follows the unit on resale. |

| 12 | Home-country tax surprise | UK/DE/AU residents taxed on worldwide rental. Gross 7% becomes net 3.5% if not structured pre-purchase. |

Thai defamation law treats published criticism of named businesses as strict-liability. Patterns travel further than names — the same twelve identify the next decade’s problem projects, not just this one’s.

Request the title document and the foreign-quota register from the Land Office. Match parcel ID, area in rai, and current encumbrances against the marketing plan. Ten-minute job; eliminates risks 2, 3 and 9.

Walk through one already-handed-over project from the same developer. Talk to two owners. If there is no completed project, the developer is the experiment — and you are funding it. Eliminates risk 7.

Ask for the escrow agreement, the bank reference, and the construction-milestone draw schedule. Refuse single-account holding. Match payment currency to invoice currency at BoT mid-rate. Eliminates risks 6 and 8.

Compare the guaranteed return against three comparable hotel-managed buildings in the same district, using STR Global ADR data. A guarantee more than 200bps above benchmark is paid by future buyers. Eliminates risks 4 and 5.

Thai law gives a foreigner two clean ways to hold residential property on Phuket. Each one is a different instrument with different cash-flows, exit mechanics and resale audience.

| Attribute | Freehold condo | Leasehold villa |

|---|---|---|

| Legal basis | Condominium Act B.E. 2522 (1979, as amended) | Civil & Commercial Code §§540–571 |

| Registered title | Chanote in foreigner’s name, on the foreign-quota register | Land remains with Thai owner; lease registered against the Chanote |

| Term | Perpetual | 30 years (statutory max), renewals contractual only |

| Resale audience | Anyone, foreign or Thai (subject to quota) | Mostly fellow foreign investors; thinner pool |

| Inheritance | Direct, by Thai will or home will | Lease transferable only with landlord consent |

| Foreign quota cap | 49% of saleable area | Not applicable |

Freehold rewards a holder who values resale liquidity and inheritance simplicity. Leasehold rewards a holder who values land use, privacy and lower headline price — and who plans to consume the asset rather than trade it.

Brokers describe leasehold as “ninety years.” The Land Office registers thirty. Everything beyond lives in a private contract.

Section 540 of the Civil & Commercial Code caps a registered lease at thirty years. Longer periods are reduced by law to thirty. The Land Office stamps one term, no more.

The two further thirty-year tranches are renewal options — personal undertakings, not registered property rights. Enforceability depends on the landlord still existing, solvent and willing, or on a structure that survives them.

Thai Supreme Court rulings (Dika decisions of 2008 and 2017) have held that an unregistered renewal does not automatically bind a successor landlord — the new buyer takes free of the personal promise.

A freehold building loses value through wear, fashion and oversupply. A leasehold building loses value through wear, fashion, oversupply and the calendar. The fourth factor is the one buyers misprice.

| Years remaining on lease | Resale discount vs new | Buyer pool |

|---|---|---|

| 30 yrs (year of registration) | 0% | Full investor pool |

| 20 yrs remaining | 15‑25% | Mid-horizon investors only |

| 10 yrs remaining | 40‑55% | Short-let operators & lifestyle buyers |

| 5 yrs remaining | 65‑80% | End-users who plan to consume the lease |

The discount accelerates because each year removed cuts both the residual cash-flow window and the buyer pool willing to underwrite renewal risk. The curve is convex, not linear.

Treat the lease the way an aircraft lessor treats a long-term operating lease: positive yield in the early decades, planned terminal value of zero. If the renewal succeeds, you have a windfall. If it fails, you were paid to live there. Both outcomes are acceptable; surprise is not.

Behind every advert in Phuket sits one of three holding structures. Each one has a setup cost, an annual cost, an exit cost, and a reputational temperature with Thai authorities. Choose on the totals, not the headline.

| Route | Best for | Setup | Annual | Regulator stance |

|---|---|---|---|---|

| Foreign quota condo | First-time foreign buyer, single asset, simplicity | USD 1.5‑3K | USD 0.2‑0.5K | Fully clean; encouraged path |

| Thai company Ltd. | Multiple villas, mixed-use, ops-active holding | USD 3‑6K | USD 1.5‑3K | Scrutinised since 2018 nominee crackdown |

| Lease + offshore (BVI) | HNW family office, inheritance planning, estate consolidation | USD 8‑15K | USD 3‑6K | Permitted; BoT & AML disclosure required |

Setup includes legal drafting, registration fees and any company incorporation. Annual covers accounting, statutory filings, secretarial services and director fees. Exit, not shown, runs USD 1–5K for the condo route, USD 3–8K for a clean company wind-down, and USD 5–12K for an offshore unwind — assuming all filings are current. Distress-exit costs are several multiples of these; the number you see is the disciplined-exit number.

For two decades the Thai company was the standard answer when a foreigner wanted to hold land. A 51% Thai shareholder, a 49% foreign shareholder, foreign-controlled operations. The structure still exists. The risk profile does not.

From 2018 onward the Department of Business Development (DBD) began auditing land-holding companies whose Thai shareholders showed nominee indicia: no traceable income to fund the subscription, no activity beyond the holding, shared address with the foreign principal. Between 2022 and 2024 the Revenue Department (RD) opened a parallel front, scrutinising the same structures for unreported beneficial ownership, related-party transactions and dividend flows. Today a land-holding company that draws DBD attention almost always draws RD attention shortly after — and vice versa. The Foreign Business Act B.E. 2542 (1999) was already on the books; what changed was the willingness of two ministries to enforce it together.

A Thai company that owns land is legitimate when its Thai shareholders are real, substantial and independent. Family-business partnerships, JVs with established Thai operators, and onshore funds with genuine Thai LPs all clear the bar.

A first-time buyer with no Thai counterparties carries the whole nominee risk on a structure designed for shared economic interest. The structure should follow the operating model, not the other way around.

The same island, the same district, the same price band — two buyers, two correct answers. The structure follows the buyer’s balance sheet, hold horizon and inheritance plan, not the developer’s preference.

Single-asset buyer, USD 650K budget, ten-year horizon, no Thai operations, lives in London. Inheritance handled by a UK will. Bought one branded freehold condo in Bang Tao under the foreign quota. Total holding-cost overhead: USD 0.4K per year. Resale audience: every foreign and Thai buyer in the building’s 49% slice. The structure disappeared into the asset.

Four-villa programme, USD 14M commitment, 25-year horizon, family-trust beneficiaries across three jurisdictions. Land registered in a Thai company with substantive Thai partners; long leases held by a BVI vehicle; BVI shares held by the family trust. Annual overhead: USD 6–9K. Inheritance settled at trust level — no Thai probate. The structure does work that the asset alone cannot.

A BVI overlay costs roughly USD 5K per year against any single asset. On one condo it is dead weight; on a portfolio with succession needs it is the cheapest layer in the stack. Run the cost against what the structure actually delivers — resale liquidity, tax efficiency, inheritance — before subscribing to it.

Across 299 tracked transactions, median time from first enquiry to handover ran 4–5 months for a ready condo and 9–12 months for a villa under construction.

| # | Step | Time | Remote? |

|---|---|---|---|

| 01 | Discovery — profile, budget, hold horizon | 1‑2 wks | Yes |

| 02 | Long-list — 8–12 candidates benchmarked | 1 wk | Yes |

| 03 | Short-list — site visits, 3–5 finalists | 1‑2 wks | Strongly no |

| 04 | Due diligence — title, developer, contract | 2‑3 wks | Yes (lawyer) |

| 05 | Reservation — deposit, refund window | 1‑3 days | Yes |

| 06 | SPA signing — milestones, FX, force majeure | 2‑4 wks | Yes (PoA) |

| 07 | Transfer — Land Office, FX proof, snagging | 1‑3 days | Yes (PoA) |

Six of seven steps run on email and electronic transfer. Step 03 — site visits — is the one that needs your physical presence. Compress it to a single five-day trip and the rest of the timeline collapses cleanly around it.

Headline price is one number on the brochure. Total cost-to-keys is six numbers, paid at six different points to six different counterparties. Buyers who model only the headline are unpleasantly surprised at the closing table.

| Cost line | Paid to | % of price | When |

|---|---|---|---|

| Reservation deposit | Developer / escrow | 1‑3% | Step 05 |

| Legal & due diligence | Independent Thai counsel | 0.5‑1.0% | Step 04 |

| Transfer fee (split) | Land Office | 1.0% | Step 07 |

| Specific business tax + stamp | Land Office | 0.5‑3.3% | Step 07 |

| Sinking fund + first-year CAM | Building / juristic person | 1‑2% | Step 07 |

| FX & FET form processing | Receiving Thai bank | 0.1‑0.3% | Step 06‑07 |

| All-in friction over headline | 3‑7% | By Step 07 | |

Transfer fee and specific business tax are statutorily split 50/50 between buyer and seller, but who pays what is contractually negotiable and varies by project. New launches in soft markets often advertise “all closing costs covered.” Resale transactions almost never do. Always price the friction at the upper end of the range until the SPA confirms otherwise — the discipline costs nothing and removes a frequent late-stage surprise.

The same seven steps can take four months or eleven. The variable is rarely the developer; it is the buyer’s preparedness and the structure being built. Two composite cases below, both drawn from MORE Group’s 2024–2025 advisory pipeline.

A Manchester engineer, 38, single freehold condo in Bang Tao for personal use plus off-week rental. Profile clarified week two; long-list week three; flew in for a five-day visit in week five and short-listed two projects; due diligence completed week eight; reservation week nine; SPA signed week eleven by PoA; Land Office transfer week sixteen. Four months end-to-end, of which four weeks were waiting on the developer’s legal team.

A Zurich couple acquiring a leasehold villa in a closed estate, lease wrapped under a BVI overlay for inheritance. Discovery and structuring ran six weeks — the offshore vehicle needed family tax-counsel sign-off. Construction at 35% at reservation, so SPA payments milestoned across nine months. Land Office registration of the lease and the BVI added three weeks. Total: eleven months, of which under two weeks were on the island.

Case B was triple Case A in dollars and elapsed time — the multiplier came from layered structure (BVI + lease + Thai land) and staged construction, not from anything inherent to villa-buying.

A Phuket residential purchase rests on four documents. Two carry money, one carries authority, one carries recurring obligations. Each one rewards a slow read.

| Document | Function | Where it lives after signing |

|---|---|---|

| Reservation Agreement | Locks the unit, sets the deposit, defines the refund window | Developer file; rarely registered |

| Sales & Purchase Agreement (SPA) | The contract: payment milestones, defect liability, force majeure, exit | Developer + buyer; basis for Land Office filing |

| Sinking Fund & CAM Agreement | Common-area maintenance rates and sinking fund contribution | Juristic person of the building; binds successors |

| Power of Attorney | Delegates signing authority to your Thai counsel for closing | Thai consulate / Land Office; narrowly scoped |

The PoA is one page and matters most for control. The CAM is two pages and matters most for cost. The SPA is fifteen and matters most for exit. The Reservation is half a page and decides whether your deposit comes back. Read the short ones twice.

A standard Phuket SPA runs fifteen pages. Most is boilerplate. Five clauses do the work; if they are wrong, no headline price-cut compensates.

| Clause family | What the clause is really agreeing to |

|---|---|

| 1. Payment milestones | Whether your money is staged against verifiable construction — or the developer’s calendar regardless of build state. Insist on third-party engineer sign-off per tranche. |

| 2. Force majeure | Whether strikes, regulatory change or a soft market relieve the developer of liquidated damages. Generic clauses give them the upside; tight clauses preserve yours. |

| 3. Defect liability | How long the developer is on the hook for structural and finishing defects. Thai market default is one year structural / three months snagging — weak. The institutional benchmark MORE Group negotiates toward is 5 years structural / 1 year finishes. |

| 4. Operator override | Whether the developer can change the hospitality operator post-handover without owner vote. If yes, your projected yield rests on a counterparty you did not choose. |

| 5. Exit & resale | Right of first refusal on resale, sub-leasing restrictions, exit fees. Each one narrows your future buyer pool. |

Developers concede on volume, not on detail. Pick the three clauses that matter most to your hold thesis — usually milestones, defect liability and operator override — and negotiate those firmly. Fighting all five at once tells the developer you do not yet know which battle you are in.

Most red flags are negotiable; a few are structural. The three patterns below cannot be drafted around — they reveal a counterparty misaligned with you from day one.

The deposit converts to non-refundable on signature with no link to the developer delivering clean title, permit or escrow reference. This monetises indecisive buyers; serious developers tie irrevocability to due-diligence delivery.

Funds flow to the developer’s general account, not a segregated escrow at a Thai commercial bank. In a delay or insolvency, your money is an unsecured claim. Escrow is standard and cheap — refusal signals cash-flow stress.

The operator is named in the SPA with no owner mechanism to vote them out. Your projected yield becomes a function of someone else’s discipline, indefinitely.

Rising markets tempt buyers to overlook structural clauses. They surface as exit friction and forced sales when the cycle turns.

Walk-time to the nearest swimmable beach, hill versus plain, and the visual quality of the immediate setting.

Lifestyle plazas, supermarkets, hospitals, international schools within fifteen minutes, and the airport in under an hour.

New units announced over the next thirty-six months versus current absorption. A high pipeline is a downward pressure on resale.

Tracked time-to-sale at district median, and the depth of the secondary buyer pool beyond the original developer.

Of fourteen districts MORE Group tracks, seven account for the overwhelming share of foreign investment activity. The other seven are either thinly traded, dominated by Thai owner-occupiers, or commercial in nature. The chapters that follow take each one in turn.

| District | Score | Median USD/m² | Yield | Best fit |

|---|---|---|---|---|

| Bang Tao & Layan | 8.4 | 5,400 | 6.0‑7.5% | Capital-Preserver |

| Surin & Kamala | 8.6 | 6,800 | 5.5‑6.8% | Quiet-Luxury hold |

| Patong | 7.2 | 3,900 | 7.0‑9.0% | Pure-Yield Investor |

| Rawai & Nai Harn | 7.6 | 3,400 | 5.5‑7.0% | Lifestyle-Migrator |

| Cherngtalay & Thalang | 7.4 | 2,900 | 5.0‑6.5% | Family-with-schools |

| Mai Khao & Nai Yang | 7.9 | 4,200 | 6.2‑7.8% | Early entry, branded |

| Phuket Town | 7.0 | 2,400 | 4.8‑6.0% | Diversifier, low-tourist beta |

A 7.0 can beat an 8.4 for the right profile. The chapter decides the fit.

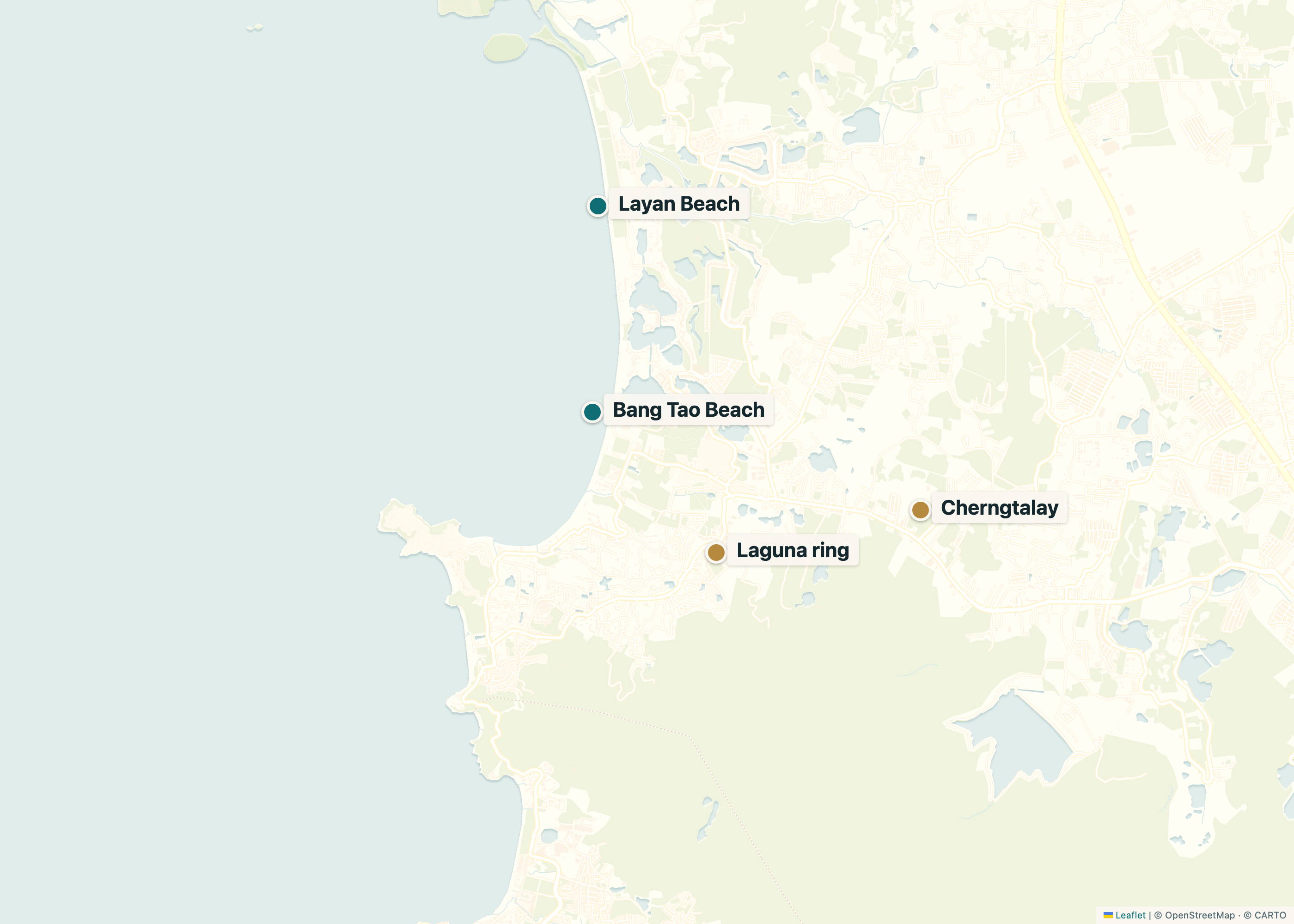

From the air, Bang Tao reads as one continuous belt of low-rise resorts. On the ground it is three sub-markets with different price ladders, different tenant pools and different exit profiles.

| Micro-area | Character | USD/m² | Buyer brief |

|---|---|---|---|

| Layan beach belt | Quietest stretch, low-density villas and ultra-prime condos against a national-park boundary. | 7,500‑11,000 | Family hold, low rental, capital preservation. |

| Laguna ring | Master-planned resort lagoon: branded residences, golf, hotel-managed pools. | 5,000‑7,500 | Hotel-managed yield, lifestyle use four to six weeks a year. |

| Bang Tao village & Boat Avenue | Walkable plaza district, supermarkets, restaurants, denser low-rise condo stock. | 3,500‑5,000 | Long-stay rental, snowbird demand, lower entry price. |

Three reinforcing factors keep Bang Tao at the top of the atlas. The beach is wide and north-facing. The infrastructure spine behaves more like an urban district than a resort. And almost every international branded operator has either landed here or is in active marketing within five kilometres. The premium is real; so is the floor under it.

The headline yield range hides three different rental engines. Pulled apart, it changes which building you should buy.

| Building category | ADR USD | Occupancy | Net yield | Operator share |

|---|---|---|---|---|

| Branded hotel-managed condo | 320‑480 | 68‑76% | 6.5‑7.5% | 50/50 to 60/40 (operator/owner) |

| Independent condo, professional manager | 180‑260 | 62‑70% | 5.5‑6.5% | 15–25% to manager |

| Pool villa, agency-managed | 450‑900 | 45‑55% | 4.5‑5.5% | 20–30% to agency |

A London-based family office acquired two units in a hotel-managed branded residence in the Laguna ring in 2023, total ticket close to USD 3.6 M. Year-three blended net yield, post fees and CAM, is tracking inside the upper half of the branded category. The decision filter at acquisition was not the brand. It was the operator’s standing reservations book and the ability to lock a fixed maintenance scope for the first ten years.

The pattern repeats across the sample. Branded clears the top of the band; independent lands in the middle; villas trade yield for use.

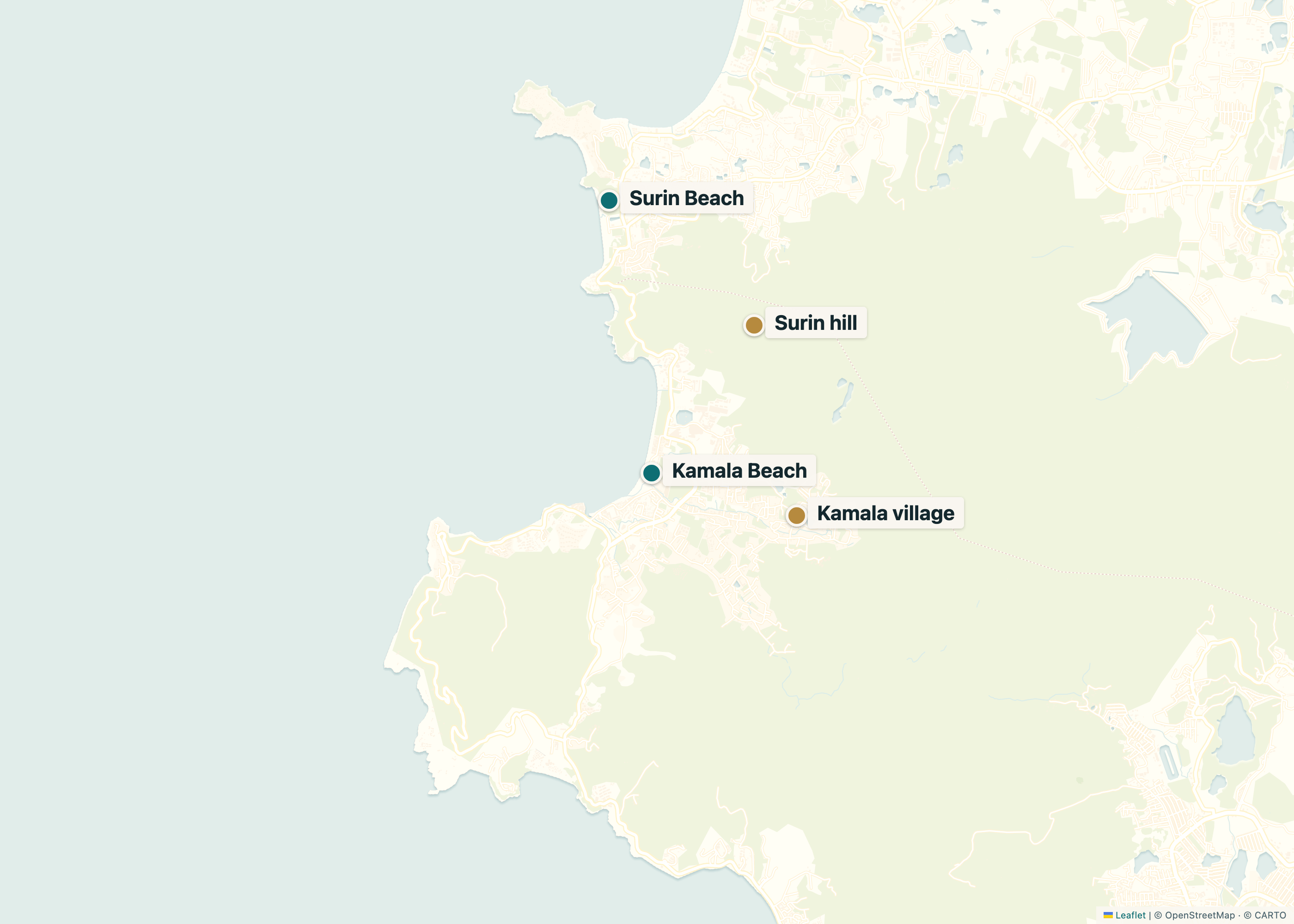

Surin and Kamala sit either side of a single headland. They share a buyer profile and a structural constraint: very little new beachfront land remains available, and the planning environment is unlikely to release more.

| Sub-area | Character | USD/m² | Stock type |

|---|---|---|---|

| Surin headland | Cliffside villas, ultra-prime branded condos, calm-water bay. | 8,000‑14,000 | Villas, low-rise condos. |

| Surin hill | Inland villa belt with a five-minute beach descent. | 4,500‑6,500 | Pool villas, mid-rise condos. |

| Kamala beach | Wide bay, moderate density, established branded resorts at both ends. | 5,500‑8,500 | Branded condos, hotel-managed. |

Both villages are pinned between sea and protected hillside. Add national-park boundaries and a long-standing reluctance from local authorities to upzone, and the result is a shrinking pipeline of new beachfront product against a steady inflow of European and Singaporean buyers who have known these beaches for two decades. That dynamic does most of the price work.

It also explains the lower yield. Buyers solve for resale to someone like them, ten years out.

Tracked transactions in Surin and Kamala over the last thirty-six months cluster into three pockets. The numbers below are the disciplined-exit ones, after operator fees, sinking fund and CAM.

| Ticket USD | Net yield | Hold | Buyer profile | |

|---|---|---|---|---|

| Cliff villa, Surin | 3.5‑7.0 M | 3.5‑5.0% | 10 yr+ | European family, primary use. |

| Branded condo, Kamala | 0.9‑2.5 M | 5.5‑6.5% | 5‑8 yr | Singapore / HK investor, mixed use. |

| Hill villa, Surin | 1.2‑2.8 M | 4.5‑5.5% | 7‑10 yr | UK lifestyle migrant, long stays. |

A Singapore-based couple acquired one cliff villa in Surin for personal use and one branded Kamala unit on a managed program. The villa carries the family. The condo carries the holding cost. The combined position runs cash-positive on year-three figures while letting them spend ten weeks a year in their own house. The structural decision was treating the two assets as a single portfolio with one balance sheet.

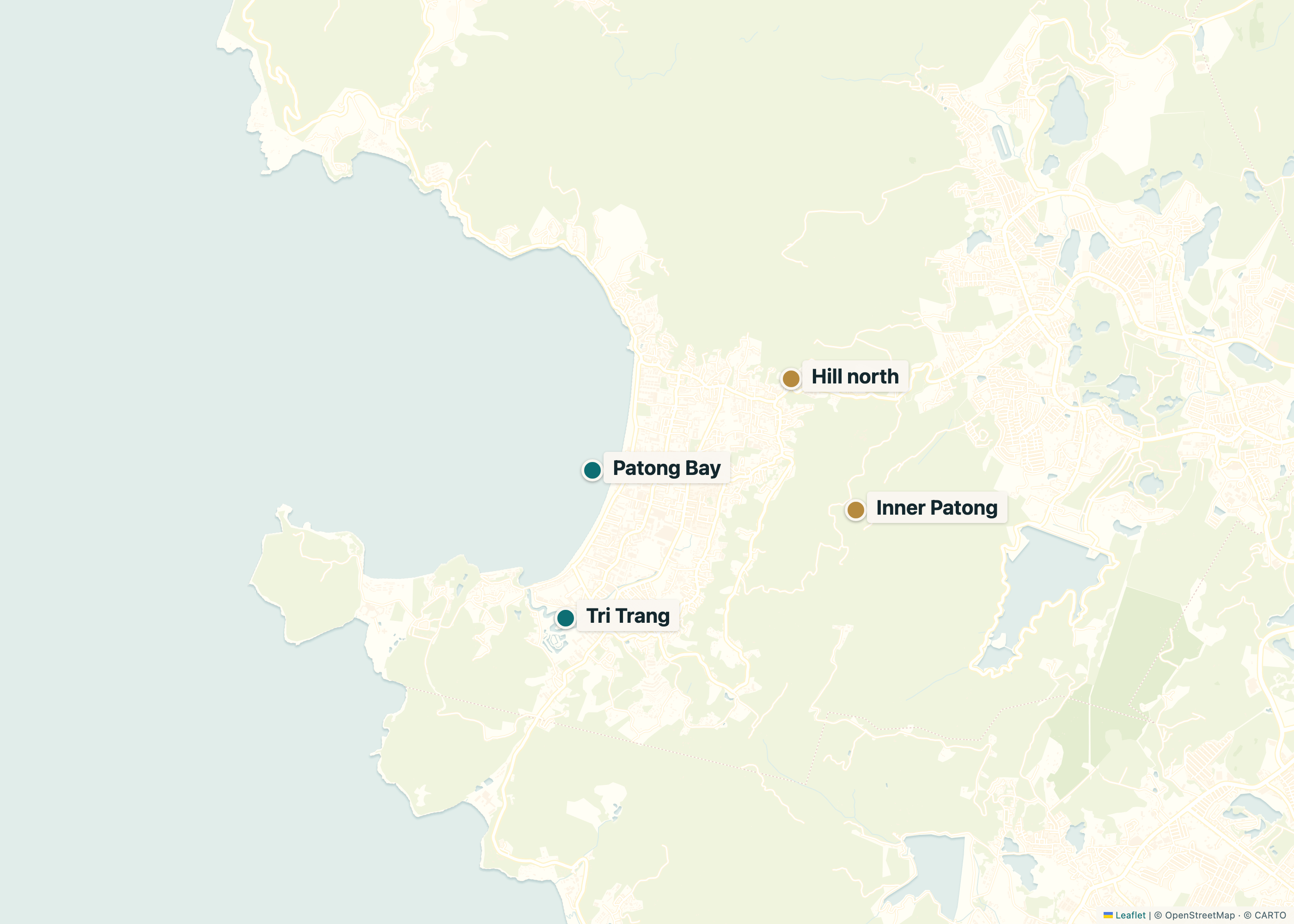

Patong is the only district on Phuket where occupancy stays above sixty per cent through the green season. The bay carries the lowest seasonality, the deepest hotel infrastructure and the heaviest short-let demand. That combination prices into rental yield, not into capital value.

| Building category | ADR USD | Occupancy | Net yield | Manager |

|---|---|---|---|---|

| Branded condotel, sea view | 160‑240 | 75‑82% | 7.5‑9.0% | Hotel operator, fixed split. |

| Independent condo, hill | 90‑140 | 68‑75% | 6.5‑7.5% | Local manager, 20–25%. |

| Studio block, Patong inner | 55‑90 | 72‑80% | 7.0‑8.0% | Self-managed or platform-based. |

Patong is rarely a personal-use asset. The traffic, the sound profile and the density that make it a hospitality engine make it a difficult holiday base for a family. The disciplined Patong buyer treats the unit as a yield instrument with a defined hold — usually five to seven years — and exits before the building’s first major refurbishment cycle, when CAM step-ups begin to compress net yield.

Bought as a hospitality asset and exited on the same logic, Patong remains the best yield district on the island. Bought as a beach apartment, it consistently disappoints.

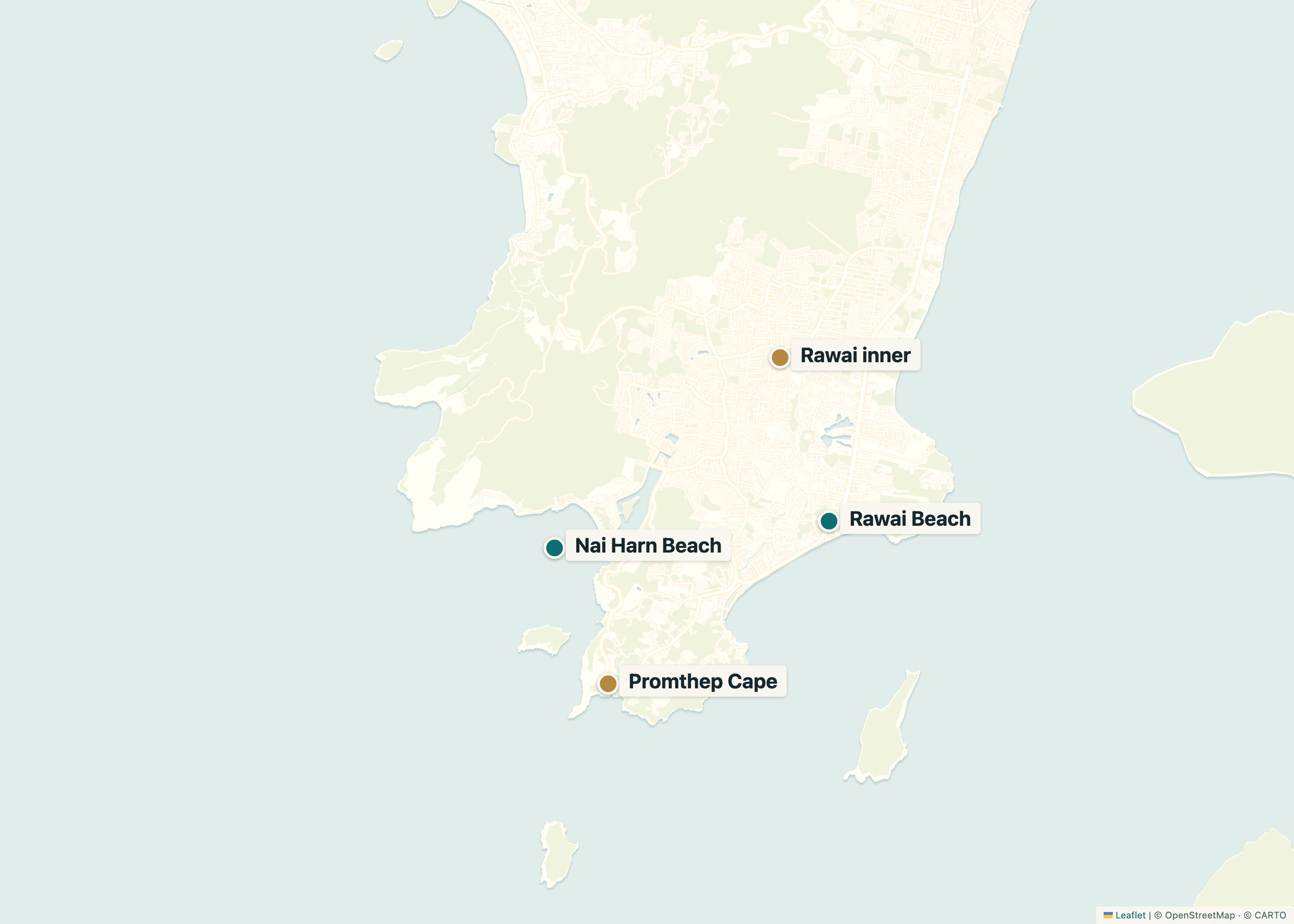

Rawai and Nai Harn carry the most established long-term foreign community on Phuket. That community is the asset. It explains why villas trade thinner than condos, why six-month leases anchor the rental market, and why personal-use buyers cluster here.

| Product | Ticket USD | Net yield | Hold | Typical buyer |

|---|---|---|---|---|

| Pool villa, inland | 450K‑1.1M | 4.5‑6.0% | 7‑12 yr | European retiree or remote worker. |

| Beachfront condo | 280K‑650K | 5.5‑7.0% | 5‑8 yr | Mixed-use lifestyle owner. |

| Townhouse, Rawai inner | 220K‑380K | 5.0‑6.5% | 6‑10 yr | Family relocating, school-distant. |

A founder relocating partly from Brussels acquired a three-bedroom pool villa in inland Rawai in 2023 at USD 640K, leasehold structure with renewal protection in the SPA. He spends six months a year on the island, lets the villa for the remaining four to six months on six-month corporate stays. Year-three blended cash position is roughly break-even after costs — the asset works as a subsidised second home rather than a yield instrument. That is the honest framing for the district.

Drive a fifteen-minute radius around three large international schools and you will sit inside the highest concentration of Western family demand on Phuket. The product reflects that demand: townhouses, three-bed villas, and family-format condos built on family budgets.

| Product | Ticket USD | Net yield | Hold | Demand engine |

|---|---|---|---|---|

| Townhouse, 3-bed | 230K‑380K | 5.5‑6.5% | 5‑8 yr | Annual school-year leases. |

| Family villa, pool | 450K‑850K | 5.0‑6.0% | 7‑10 yr | Two-year corporate leases. |

| Family condo, 3-bed | 320K‑560K | 5.0‑6.0% | 5‑8 yr | Mixed lease & owner use. |

There is no beach inside Cherngtalay or central Thalang. The visual product is sub-tropical, ordinary, often unremarkable. The fundamentals are anything but. Long-term lease demand from families on multi-year postings carries a much lower volatility than the short-let market, and the school anchors create a structural floor under tenant churn. The asset class trades like a piece of Singapore suburban housing rather than like a Phuket holiday product, and that is its quiet strength.

For a buyer who can read past the photos, this is one of the most defensible districts on the island.

For a long time the north coast carried a single label: too close to the airport. Two structural changes have rewritten the file. First, several internationally branded resort operators have opened five-star properties along the Mai Khao stretch. Second, the airport upgrade and the planned light-rail trunk line shorten the perceived distance to the rest of the island.

| Product | Ticket USD | Net yield | Hold | Thesis |

|---|---|---|---|---|

| Branded condo, Mai Khao | 350K‑750K | 6.5‑7.5% | 5‑8 yr | Pipeline-led re-rating. |

| Pool villa, Nai Yang inland | 280K‑520K | 5.5‑6.5% | 7‑10 yr | Lifestyle, low entry. |

| Beach condo, Nai Yang | 180K‑320K | 6.0‑7.0% | 5‑7 yr | Short-let to airport traffic. |

The same operator influx that drives the rerating will, over five years, raise district supply by an estimated thirty to forty per cent. Buyers entering early benefit. Buyers entering after the supply lands will find themselves competing for the same hotel-managed booking pool against a wider stock. The structural answer is to buy product with a credible operator now and to set the exit clock against the pipeline curve, not the price curve.

Phuket Town does not compete with the beaches. It complements them. The asset profile is closer to a small Asian secondary city than to a resort — long-term tenants, civic infrastructure, lower seasonality and a domestic Thai professional buyer base that thickens the secondary market.

| Product | Ticket USD | Net yield | Tenant pool | Correlation to coast |

|---|---|---|---|---|

| Old Town shophouse, restored | 320K‑750K | 5.5‑6.5% | Cafe / boutique tenant. | Low |

| Mid-rise condo, civic centre | 120K‑240K | 6.0‑7.0% | Thai professional, annual lease. | Very low |

| Townhouse, suburban Phuket Town | 160K‑280K | 5.5‑6.5% | Local family. | Very low |

For a portfolio with three or more west-coast resort assets, adding a Phuket Town line at five per cent of total weight reduces the portfolio’s sensitivity to a tourist-arrivals shock by a meaningful, measurable amount — without dragging blended yield. The role is hedge, not hero. Buyers who size it as a hero are usually disappointed; buyers who size it as a hedge are usually surprised by how reliable it becomes.

Phuket sells essentially three residential products to foreigners: a foreign-quota condominium, a leasehold villa, and a townhouse on a long-lease structure. They look like a spectrum of size and price; in practice they behave like three different asset classes.

| Attribute | Foreign-quota condo | Leasehold villa | Townhouse (lease) |

|---|---|---|---|

| Typical ticket (USD) | 120K‑1.5M | 0.7‑6.0M | 180K‑500K |

| Title structure | Freehold inside 49% quota | Leasehold 30+(30) on land | Leasehold 30+(30) on land |

| Yield engine | Hotel-managed pool, daily rate | Long-let or owner use | Annual lease, family tenant |

| Net yield (typical) | 5.5‑8.0% | 3.5‑5.5% | 5.0‑6.5% |

| USD per usable m² | 3.6K‑9.0K | 3.0K‑7.5K | 2.0K‑3.5K |

| Time on market at exit | 3‑6 mo | 9‑18 mo | 6‑12 mo |

| Owner-use factor | Low (operator override) | High (your roof, your rules) | Medium (tenant-driven) |

| Annual cost stack (% of value) | 1.4‑2.2% | 2.0‑3.5% | 1.6‑2.4% |

Net yield is not a fixed property of an asset class — it changes with hold period and operating mode. The pattern below comes from MORE Group’s thirty-six-month rolling tracker across 299 active foreign-owned properties. Round to two decimal places, ignore individual outliers, and the shape of each curve is remarkably stable.

| Year | Branded condo | Indep. condo | Villa, long-let | Townhouse |

|---|---|---|---|---|

| Year 1 · ramp-up | 3.5‑5.0% | 2.5‑4.0% | 2.0‑3.0% | 3.5‑4.5% |

| Year 3 · operating norm | 5.5‑7.0% | 4.0‑5.5% | 3.5‑5.0% | 5.0‑6.0% |

| Year 5 · asset matures | 6.0‑7.5% | 4.5‑6.0% | 4.0‑5.5% | 5.5‑6.5% |

| Year 7‑8 · refit cycle | 5.0‑6.5% | 4.0‑5.0% | 4.0‑5.0% | 5.0‑6.0% |

| Year 10+ · post-refit | 5.5‑6.5% | 4.5‑5.5% | 3.5‑5.0% | 5.0‑5.5% |

Three patterns repeat. Branded condos peak in years three to five and dip during the seven-year refit cycle, then recover near the long-run mean. Villas trade yield for owner-use and capital appreciation. Townhouses behave like a stable, income-only line item.

Read the curve, not the year. Underwriting on year-three alone overstates a branded condo by roughly 120bps. Use the rolling five-year mean from year three onward.

The product type follows the buyer profile, not the other way round. Five honest questions, asked in this order, route ninety per cent of foreign buyers to the right asset class within twenty minutes.

| Question | If yes → tilt | If no → tilt |

|---|---|---|

| 1. Will you spend more than twelve weeks a year on site? | Villa or townhouse | Condo (operator-managed) |

| 2. Is annual cash flow the primary metric? | Branded condo or townhouse | Villa is permissible |

| 3. Do you have school-age children who will be on island during term? | Townhouse or villa, Cherngtalay axis | Beach-axis condo |

| 4. Is exit liquidity within 5 years a hard requirement? | Branded condo, beach district | Villa is acceptable |

| 5. Do you want privacy as the dominant amenity? | Villa, Layan / Surin / Rawai | Condo or townhouse |

Three buyer-asset matches account for the bulk of healthy transactions: capital preservers in branded condos along the Bang Tao‑Surin‑Patong axis (USD 320K‑750K); lifestyle migrants in Cherngtalay/Rawai/Thalang townhouses or three-bed villas (USD 260K‑1.4M); trophy holders in sea-view leasehold villas across Layan, Surin and Kamala (USD 1.8M‑6.0M).

Townhouse beats villa, same budget. At USD 450K, a 3-bed Cherngtalay townhouse clears 9‑11 rented months on annual leases; a comparable villa clears 5‑7 on holiday lets at higher cost. Pick by the cash, not the photograph.

Beach access, micro-area trajectory, infrastructure pipeline, school and hospital proximity. Anchored to the seven-district atlas in Part III.

Years in market, completed-versus-announced ratio, capital structure, partnerships with hotel operators or BOI affiliations. Public-record only.

Layout efficiency, ceiling height, view-line, finish-grade benchmark, common-area amenity-to-unit ratio, and building-management contract.

Price per usable m² against district median, payment schedule front-loading, rental-program transparency, exit-cost stack and capital repatriation pathway.

Calibrated against MORE Group’s rolling pipeline of 299 active properties as of Q1 2026. The 7.5 threshold marks the line below which historical resale liquidity drops sharply.

| Score band | Share | What it means in practice | Resell time |

|---|---|---|---|

| 9.0‑10.0 · conviction | 3.7% | Recommended without caveat. Brokerage often closes off-market. | 2‑4 mo |

| 8.0‑8.9 · strong | 11.4% | Recommended; minor structural caveats discussed in writing. | 3‑6 mo |

| 7.5‑7.9 · pass threshold | 9.0% | Recommended only with profile-fit match; the floor of our shortlist. | 5‑9 mo |

| 6.5‑7.4 · conditional | 22.7% | Off the shortlist. Used as comparables and for negotiation context. | 9‑15 mo |

| 5.5‑6.4 · below floor | 31.1% | Tracked for market intelligence. Not introduced to clients. | 12‑24 mo |

| <5.5 · declined | 22.1% | Excluded from pipeline. Source records retained for pattern analysis. | 18 mo+ |

Two patterns are worth flagging. The conviction tier is small by design — if it grows above five per cent of the pipeline, calibration drifts and we re-anchor. And the gap in resale time between 7.5 and 7.4 is roughly four months on average. The threshold tracks a measurable break in liquidity, not a marketing line.

The score predicts relative ranking, not an absolute return number. A 8.4-rated property may underperform a 8.0-rated peer in any year; the score asserts only that across many years the higher-rated cohort outperforms.

An anonymised real example from MORE Group’s Q1 2026 pipeline. The unit is a 1-bed, 56 m² net usable, sea-view branded condominium on the Bang Tao crescent. Walked through the framework end-to-end, with the inputs that produced each score on the 1‑10 scale.

| Factor | What we measured | Rating | Weight | Contrib. |

|---|---|---|---|---|

| Q · Location | Beach 350m, infra pipeline 2026‑28, schools 12 min. | 8.5 | 0.30 | 2.55 |

| D · Developer | Eleven completed projects, hotel operator contracted, BoI current. | 9.0 | 0.25 | 2.25 |

| A · Asset | Efficiency 87%, ceiling 2.9m, view-line clear 10+ yr. | 8.0 | 0.25 | 2.00 |

| F · Financial | Price USD 6,250/m² (+4% vs median), operator 30%. | 7.5 | 0.20 | 1.50 |

| MORE Investment Score | 8.30 | |||

The score lands in the 8.0‑8.9 band — strong, recommended with caveats. Both caveats sit in F: four per cent over district median, operator share at the high end. Sensitivity: if operator rose to 40%, F drops to ~6.0 and total to 8.00 — floor of the band.

Brochures quote a single number for area. Underneath sit three different surfaces — the gap decides whether you bought sixty square metres or forty-eight.

| Term | What it includes | What it conceals |

|---|---|---|

| Sellable area (GSA) | Apartment perimeter, including external walls, balconies and partitions. | Up to 14‑18% of the headline number is wall, ledge or open balcony. |

| Conditioned area | Indoor space heated, cooled or humidity-controlled. | Service yards, storage cupboards and outdoor decks excluded. |

| Net usable area (NSA) | Floor area you can place furniture on, walk through, or live in. | The honest number for value-per-m² comparison. |

The single most useful number is net usable divided by gross sellable. Rarely printed, always calculable. The pattern across 120+ condominiums MORE Group has audited:

| Product type | Poor (avoid) | Median | Premium |

|---|---|---|---|

| Studio, branded condo | <78% | 82‑85% | 88%+ |

| 1-bed, branded condo | <80% | 84‑87% | 90%+ |

| 2-bed, branded condo | <82% | 85‑88% | 91%+ |

| 3-bed, villa | <75% | 78‑82% | 85%+ |

A trained eye covers a floor plan in roughly twelve minutes. The eight checks below catch the value-destroying mistakes that cluster in Phuket developments.

| # | Inspection | What you are looking for | Why it matters at exit |

|---|---|---|---|

| 1 | Bathroom-to-bedroom math | 1 bath per bedroom for 2-bed+, en-suite for the master. | Family rentals price 15‑25% below comparable when ratio is wrong. |

| 2 | Kitchen-to-living separation | Closeable kitchen for villas; open-plan acceptable for studios. | Asian secondary buyers strongly prefer enclosed kitchens. |

| 3 | Door-swing geometry | Doors that do not collide with each other or block furniture. | Cumulative dead space in poor plans reaches 3‑5 m². |

| 4 | Service-yard real estate | Dedicated outdoor space for AC, washer, water heater. | Without it, these displace conditioned area on year three. |

| 5 | Storage volume | At least 1.5 m² of dedicated storage for a 1-bed. | Owner-use ratings drop sharply on properties without storage. |

| 6 | Window-to-floor ratio | Glass area at least 15% of floor area in living spaces. | Below this, units list 8‑12% below comparables. |

| 7 | View-line obstruction risk | Master plan with future towers between unit and view feature. | Rated views can disappear in 2‑3 yr; check the master plan. |

| 8 | Common-area allocation | Pool, gym, parking m² per unit, paid for by you. | Sinking fund and CAM scale with this number. |

Apartments below 2.7m ceiling read cramped — the same unit at 3.0m lists for 8‑14% more per usable m². Ask for the section drawing, not just the plan view.

A composite from the MORE Group product committee: two 2-bed condos on the same Bang Tao crescent, listed within a fortnight at indistinguishable prices. The plans did not match the brochures.

| Spec | Unit A · efficient | Unit B · wasteful | Difference |

|---|---|---|---|

| Sellable area | 82 m² | 82 m² | 0 |

| Net usable | 71 m² | 62 m² | +9 m² |

| Efficiency ratio | 87% | 76% | +11pp |

| Bedroom-to-bath ratio | 2:2 | 2:1 | Family-friendly |

| Storage | 2.4 m² | 0.4 m² | +2.0 m² |

| Window-to-floor | 19% | 12% | +7pp |

| USD price | 485K | 485K | 0 |

| USD per net usable m² | 6,830 | 7,820 | −13% |

| Indicative resale · year five | USD 610K | USD 505K | +USD 105K |

The headline price was identical; the lived experience and the secondary-market value were not. Unit A reads like a 2-bed in photographs and in person. Unit B reads as a 2-bed only in photographs — and five years later the secondary market re-priced the difference without negotiation.

A 65‑m² 2-bed at 87% efficiency provides almost the same usable area as an 80‑m² 2-bed at 72% — for less price, lower CAM and lower furnishing cost. Square metres are not the answer; usable square metres are.

A printed list of named buildings is obsolete the day it ships — new towers complete, operators change, ownership rotates. Patterns last longer. The twenty-five archetypes that follow are the recurring shapes MORE Group has scored at 7.5+ across 299 active properties, distilled to the structural traits that produce the score.

| Field | What it means |

|---|---|

| ID | An internal reference (A01‑A25). No relation to project names. |

| District | One of the seven districts mapped in Part III. |

| Type | Branded condo, independent condo, leasehold villa, townhouse, or shophouse. |

| Ticket range (USD) | Where this archetype typically transacts; midpoint is the best planning anchor. |

| Net yield (typical) | Year-three to year-five mean, post all operator and ownership cost. |

| MORE Score | The four-factor score (Ch. 18) for the median example in this archetype. |

| Why it’s on the list | The structural reason this pattern earns its place — not the marketing pitch. |

| Key risk to watch | The single failure mode that historically takes this archetype out of band. |

None of the twenty-five entries names a developer, project, operator or broker. The underlying buildings exist; the printed list does not point at any of them. Live introductions happen one-to-one, on the call that follows the book.

The shortlist intentionally spreads across districts, ticket sizes and product types so that the framework returns at least one strong match for any of the three buyer profiles in Chapter 17. The dashboards below summarise the spread.

| District | Archetypes | Median ticket | Median yield | Median score |

|---|---|---|---|---|

| Bang Tao & Layan | 4 | USD 540K | 6.4% | 8.4 |

| Surin & Kamala | 3 | USD 980K | 5.2% | 8.2 |

| Patong | 4 | USD 310K | 7.4% | 8.0 |

| Rawai & Nai Harn | 3 | USD 420K | 5.8% | 8.1 |

| Cherngtalay & Thalang | 4 | USD 360K | 6.0% | 8.3 |

| Mai Khao & Nai Yang | 3 | USD 440K | 5.6% | 7.9 |

| Phuket Town | 4 | USD 230K | 6.0% | 8.0 |

| Aggregate | 25 | USD 420K | 6.0% | 8.1 |

| By type | Count | Ticket band | Yield band | Best fit |

|---|---|---|---|---|

| Branded condo | 10 | USD 180K‑1.2M | 5.5‑7.8% | Capital preserver |

| Independent condo | 5 | USD 120K‑420K | 5.0‑6.5% | Yield-first, hands-on |

| Leasehold villa | 5 | USD 0.8M‑3.5M | 3.5‑5.5% | Lifestyle / trophy |

| Townhouse | 3 | USD 230K‑480K | 5.0‑6.5% | On-island family |

| Shophouse, restored | 2 | USD 320K‑750K | 5.5‑6.5% | Urban diversifier |

Bang Tao · Layan · Surin. West-coast premium — brand, scarcity, operator economics.

Why Direct sea-view inventory inside the branded operator’s pool program. Liquidity at exit is the strongest on the island; secondary market typically clears in three to five months.

Risk Future tower in the master plan can compress the view-line by year five. Verify no-build covenants before deposit.

Why Scarcity. Cliff plots adjacent to Layan beach are functionally capped by topography; the supply curve is short and certain.

Risk Lease structure: a thirty-plus-thirty with a documented renewal trigger is essential. Without it, year-twenty-five capital decay accelerates.

Why Inside the Laguna ring, infrastructure is privately maintained, school catchment is established, and the resale buyer pool is wider than for raw beachfront.

Risk Operator share at the high end of acceptable; underwrite at 35% not 30%.

Why Annual leases to expat families on academic calendar. Demand is documented by international school enrolment growth; vacancy stays near zero in the term window.

Risk Off-season cash flow if you target holiday lets instead of the school market. Pick one channel and optimise for it.

Why The benchmark trophy asset on the island. A small, fixed inventory of cliff plots; secondary market thin but consistently bid by European and Asian family offices.

Risk Year-on-year carrying cost is high; underwrite assuming sixteen weeks of personal use and the rest covered by long-let, not by holiday yield.

Kamala & Patong. Quiet luxury one side, the yield engine the other.

Why Kamala’s tighter footprint produces a slower asset, smaller buyer pool, and a price that holds. The micro-area is favoured by Asian repeat buyers, who underwrite calmly.

Risk Pool-view stacks behind sea-view stacks compress in resale faster than the headline beach premium suggests. Premium for true sea-view is justified.

Why The entry point into the Surin trophy market. A three-bed hill villa rents to long-let lifestyle migrants while compounding on the same scarcity that drives the cliff segment.

Risk Hill access roads can deteriorate; verify the road maintenance regime and budget USD 2‑4K per year for shared upkeep.

Why The yield engine. ADR 120‑220 USD, occupancy 76‑82%, full operator program, transparent statements. Capital appreciation modest; cash flow strong and predictable.

Risk Operator override on personal use can be aggressive; negotiate a documented owner-use window before signing.

Why The two-bed sea-view stack carries premium ADR even within Patong’s already premium yield curve. The asset reads as a condo, prices as a condotel, and exits to a wider buyer pool than the studio block.

Risk Patong noise envelope; verify acoustic mitigation and orientation away from the bar grid.

Why Self-managed studios in independent buildings on the Patong inner grid. Highest gross-yield archetype in the shortlist; works for hands-on owners with a local operator.

Risk Building-management quality varies sharply; the wrong juristic person collapses both yield and resale value within three years.

Patong inner · Rawai · Cherngtalay schools. Mid-tier yield, lifestyle south, academic calendar.

Why A step up from the studio block: better layouts, longer-stay tenants, slightly lower turnover cost. Yields the most stable mid-tier cash flow in the Patong segment.

Risk Foreign quota in older independent buildings can already be filled; check the quota register at the Land Office before reservation.

Why Lifestyle South’s defining product. Strong long-let demand from European founders and remote workers; community premium thickens the secondary market.

Risk Pool-pump and water-tank maintenance is structural cost; budget USD 2.5K per year before management.

Why Beach is a five- to ten-minute walk; tenants are repeat lifestyle migrants on six-to-twelve-month leases. Lower headline yield than Patong but with materially lower vacancy.

Risk Inventory is thin; competition from owner-occupiers can compress investor yield by a quarter to a third over three years.

Why Best m²-per-USD ratio in the Rawai cluster. Suits couples and small families who do not need a private pool but value the community footprint.

Risk Resale to Thai buyers is a non-trivial part of the exit pool; staging and family-friendly layout matter more than for villas.

Why Pre-let almost on completion to academic-year families. Annual leases at 10‑11 months rented; the most stable cash-flow archetype outside Patong.

Risk School calendar collapses if any of the major international schools relocates within a five-year horizon. Diversify tenants where possible.

Inland family & northern frontier. Cherngtalay families, Mai Khao and Nai Yang.

Why Larger condo footprint inside school catchment, lower friction than a townhouse, easier to manage from abroad. The closest condo product to the family-villa profile.

Risk Common-area cost scales with the family amenity stack; CAM and sinking fund will run 15‑20% above district median.

Why The price entry point for a four-bed villa with private pool. Buyer pool is dominated by relocating families and remote-working executives on multi-year leases.

Risk Ground-water and septic infrastructure in some Thalang pockets is privately maintained; survey before deposit, budget for replacement.

Why Boutique cluster of 8‑14 villas around a shared courtyard or lake. Best-in-class for community premium without the cost stack of full beachfront.

Risk Small clusters depend disproportionately on the original developer’s management hand-off; verify the juristic person is established and funded before completion.

Why Direct beachfront at a price unavailable on the central west coast. Operators run year-round programs anchored on airline crews and long-stay leisure guests.

Risk Pipeline supply over the next five years can absorb the price re-rating slowly; underwrite at year-three numbers, not at developer projections.

Why The northern alternative to Bang Tao at roughly half the price. The micro-area is favoured by repeat European visitors who underwrite calmly and stay long.

Risk Coastal-zone restrictions limit setback flexibility; verify environmental clearance and master-plan stability before any deposit.

Mai Khao pre-completion & Phuket Town. Off-plan capital play north, low-correlation urban assets in town.

Why Off-plan entry at front-loaded payment plan; capital appreciation built in if the asset completes inside the published window. Highest expected total return in the shortlist.

Risk Construction delay and developer execution; this archetype only works with a top-quartile developer record (factor D ≥ 8.5).

Why Sino-Portuguese architecture inside the heritage zone. Mixed-use ground-floor cafe or boutique plus residential upper floors; structural diversifier away from coastal seasonality.

Risk Heritage-zone restoration requirements add cost; engage a counsel familiar with Old Town conservation rules before purchase.

Why Long-let to Thai professionals; near-zero seasonality. The least correlated archetype to tourist arrivals; ideal counter-weight in a coast-heavy portfolio.

Risk Foreign quota in some Phuket Town buildings is already saturated; verify before reservation.

Why Local family tenants on multi-year leases. The most predictable cash-flow archetype on the island; behaves more like a small Asian secondary-city asset than a resort property.

Risk Capital appreciation is the slowest of any archetype here; do not size this for growth, size it for income.

Why The trophy variant of A22. Larger footprint, frontage on the gallery axis, capable of hosting a hospitality concept upstairs and a cafe or studio downstairs.

Risk Tenant concentration: the upside is amplified by a strong concept and amplified down by a weak one. Underwrite as a small business asset, not a passive condo.

Sorting the twenty-five archetypes by ticket midpoint shows yield does not rise smoothly with price. It moves in distinct bands, each driven by a different economic engine.

| Ticket band | Archetypes | Median yield | Median score | Engine |

|---|---|---|---|---|

| USD 110K‑230K | 8 | 6.6% | 7.9 | Yield engine: studios, condotels, civic-centre condos. |

| USD 230K‑480K | 10 | 6.0% | 8.1 | Balance band: branded one-beds, townhouses, family condos. |

| USD 480K‑1.0M | 4 | 5.5% | 8.3 | Family / lifestyle: two-beds, courtyard villas, three-bed townhouses. |

| USD 1.0M+ | 3 | 4.5% | 8.3 | Trophy: cliff villas, hill villas, premium leasehold. |

Yield falls as ticket rises — score does not. The highest-conviction archetypes (8.4+) cluster in two unrelated bands: Patong condotels and trophy west-coast villas. The balance band (USD 230K‑480K) is the most populated because buyer demand, operator economics and product quality intersect there most reliably.

Across the twenty-five archetypes, the correlation between USD per usable m² and the MORE Score is well under 0.40. The score makes that judgment explicit.

Six entries score 8.3+: not the most expensive, not the highest-yielding, but the archetypes where every factor sits in the upper band simultaneously.

| ID | Archetype | District | Score | The reason it earns conviction |

|---|---|---|---|---|

| A01 | Sea-view branded one-bed | Bang Tao | 8.6 | Highest exit liquidity; operator program at the strongest end of the spectrum. |

| A05 | Surin cliff villa, sunset | Surin | 8.5 | Topographic scarcity that institutional buyers underwrite without negotiation. |

| A02 | Layan cliff villa, hill | Layan | 8.4 | Smaller buyer pool than Surin but tighter supply; family-office holding asset. |

| A15 | School townhouse | Cherngtalay | 8.4 | Demand structurally locked to academic-year leases; vacancy near zero in term. |

| A09 | Patong sea-view two-bed | Patong | 8.3 | Yield engine without studio-block fragility; widest secondary-buyer pool in Patong. |

| A18 | Courtyard villa pocket | Cherngtalay | 8.3 | Community premium without coastal cost stack; small-cluster boutique pattern. |

Three traits in every entry: supply constrained by topography, setbacks, demand anchor or cluster size; operator with track record across at least one cycle; and a secondary-buyer pool diversified across geographies.

Use it to anchor what ‘very good’ looks like — not as a substitute for matching asset to buyer. A buyer’s profile can move the right answer into a balance-band or yield-engine archetype.

The shortlist gets more interesting when assembled. Three composites below show how the framework converts to a balance-sheet position. Numbers are planning anchors.

| Portfolio | ID | Archetype | Ticket | Yield |

|---|---|---|---|---|

| I · Single-asset entry Capital preserver |

A01 | Sea-view branded 1-bed, Bang Tao | USD 500K | 6.5% |

| Total | USD 500K | 6.5% | ||

| II · Yield + lifestyle Lifestyle migrant |

A08 | Patong branded condotel studio | USD 180K | 7.5% |

| A12 | Rawai inland 3-bed pool villa | USD 520K | 5.5% | |

| Total | USD 700K | 6.0% | ||

| III · Family-office Five lines, four districts |

A05 | Surin cliff villa, sunset | USD 3.8M | 4.0% |

| A01 | Sea-view branded 1-bed, Bang Tao | USD 500K | 6.5% | |

| A09 | Patong sea-view 2-bed | USD 500K | 6.0% | |

| A15 | School townhouse, Cherngtalay | USD 350K | 6.0% | |

| A23 | Civic-centre 2-bed, Phuket Town | USD 180K | 6.5% | |

| Total | USD 5.33M | 4.8% | ||

The twenty-five archetypes are a navigational instrument, not a buy list. Used in the right order, they shorten the path from preference to decision from twelve weeks to four. The sequence below is the one MORE Group runs on intake.

| Step | What you do | What we do | Time |

|---|---|---|---|

| 01 | Run the Chapter 17 decision tree honestly. Pick one buyer profile. | — | 1 hr |

| 02 | Identify three archetypes from the twenty-five that match the profile. | — | 1 hr |

| 03 | Send the three archetype IDs and your timeline to MORE Group. | We open the live pipeline filtered to those archetypes. | 1 day |

| 04 | Review the live shortlist (typically 5‑9 buildings) on a video call. | We narrate score, fit, current-quarter risk for each candidate. | 1 hr |

| 05 | Pick two buildings to inspect on island. | We coordinate access, contracts review, counsel introduction. | 1‑2 wk |

| 06 | Inspect, decide, instruct counsel. | We project-manage the seven-step buyer journey (Ch. 7). | 3‑5 mo |

This book is a framework, not a transaction. Across twenty chapters we have argued for the same discipline: read the document twice, score the property on the same scale as every other, treat the secondary buyer as your audience, match asset to engine, do not let the brochure do your underwriting. If the archetypes are useful, the next step is conversation, not commitment.

We track 299 active foreign-owned properties on Phuket. To translate any archetype into a current-quarter shortlist for your profile, write to book@moregroup.estate with the IDs and your timeline. We respond inside one working day.

There are essentially three financing routes available to a non-resident buyer. Each carries its own friction, cost, and exit profile. The choice is rarely about which is cheapest in isolation — it is about which fits the rest of the buyer’s balance sheet.

| Route | How it works | Effective rate | Setup |

|---|---|---|---|

| Pure cash | Inbound wire to escrow; FET certificate secures repatriation at exit. | — | 2‑3 wk |

| Offshore mortgage | Loan against home assets, wired to Thailand as cash. | SOFR + 1.5‑3% | 6‑10 wk |

| Developer plan | Off-plan 20/30/30/20 split across milestones. | 0% nominal | Build |

Thai banks have lent to foreign buyers in past cycles; in 2026 the practical answer for non-residents is no. Bangkok Bank’s Singapore-branch programme (active 2014‑2019) was the last meaningful onshore-funded product. UOB Thailand and Kasikorn maintain edge-case programmes for foreigners with multi-year work permits; new buyers without Thai income should not underwrite around them.

Most foreign buyers underwrite the property in their home currency and then suffer or benefit from the exchange rate when payments fall due. A USD 500K condo can become a USD 540K condo over a twelve-month off-plan schedule with no change in the Thai price tag. The currency is half the deal.

| FX strategy | Mechanics | Hedge cost | Best fit |

|---|---|---|---|

| Spot at milestone | Convert at each payment. Default. | Spread 0.5‑1.5% | Short build |

| Forward contract | Lock today for milestone delivery via broker or bank. | 0.3‑0.7% p.a. | 12‑36 mo build |

| Pre-funded THB | Park THB in non-resident baht account ahead of dates. | Carry diff. | Existing Thai bank |

| THB-denom. loan | Singapore private bank issues THB facility on home collateral. | Margin + FX | UHNW, >3M |

Working rule. If the construction schedule is longer than nine months and the ticket is above USD 300K, hedge at least half of the remaining tranche. The premium pays for itself the first time THB moves 2% against you.

Same asset — a USD 500K branded one-bed in Bang Tao, ramping from year-one yield 4.5% to year-five yield 7.0%, sold in year five at +25% nominal. Three financing routes, identical operating assumptions, real numbers.

| Outcome (5-yr hold) | Cash | Mortgage 60% @ 5.5% |

Dev plan 20/30/30/20 |

|---|---|---|---|

| Cash deployed Y0 | USD 500K | USD 200K | USD 100K |

| Annual debt service | — | USD 16.5K | — (capital instalments) |

| Net rental over 5 yr | USD 142K | USD 60K | USD 115K (starts Y2) |

| Sale proceeds Y5 | USD 625K | USD 625K − loan | USD 625K |

| Equity multiple | 1.53× | 2.42× | 2.85× |

| IRR (post-FX, post-tax) | 9.0% | 14.5% | 21.0% |

Read the table honestly. Leverage and developer plans both raise IRR by spreading capital over time — and both raise risk symmetrically. The mortgage adds rate, FX and margin-call exposure. The developer plan adds construction-completion and counter-party risk. Cash is the slowest path and the only one that survives a delivery default unhurt.

Net yield in Phuket is a function of two variables: where the asset sits and how it is operated. The matrix below is the rolling twelve-month median across 299 foreign-owned properties in MORE Group’s tracker. Net of operator share, sinking fund, CAM, insurance and Thai withholding — gross-to-net friction is real and quantified later in this chapter.

| District | Long-let (annual lease) |

Hotel-managed (branded pool) |

Self-run (short-let, owner ops) |

|---|---|---|---|

| Bang Tao · Layan | 5.0‑6.0% | 6.5‑7.5% | 5.5‑7.0% |

| Surin · Kamala | 4.0‑5.0% | 5.5‑6.5% | 4.5‑6.0% |

| Patong | 5.5‑7.0% | 7.0‑8.5% | 6.5‑9.0% |

| Rawai · Nai Harn | 5.0‑6.5% | 5.5‑6.5% | 5.0‑7.0% |

| Cherngtalay · Thalang | 5.5‑6.5% | 5.5‑6.5% | 4.5‑6.0% |

| Mai Khao · Nai Yang | 4.0‑5.0% | 5.5‑7.0% | 4.5‑6.0% |

| Phuket Town | 4.8‑6.0% | — | 4.5‑5.8% |

One pattern to read. Patong dominates yield in every operating mode — the engine is tourism volume, not asset quality. Move west-of-Patong and the operator delta narrows; move into Phuket Town and the matrix collapses to the long-let column because there is no branded pool to plug into.

A typical branded one-bed in Bang Tao priced at USD 500K with USD 42K of gross annual revenue. 8.4% on paper, 5.9% in the bank. The slippage is not theft — it is structurally where this asset class lives. Knowing the stack lets you negotiate the negotiable lines.

| Cost line | USD / yr | % gross | Negotiable? |

|---|---|---|---|

| Gross rental income | 42,000 | 100% | — |

| Operator share (pool split) | −12,600 | 30.0% | Partly |

| CAM & sinking fund | −2,800 | 6.7% | No |

| FF&E reserve (5-yr refresh) | −1,500 | 3.6% | Cap |

| Local property tax | −500 | 1.2% | No |

| Thai WHT on rental | −2,100 | 5.0% | No |

| Owner admin (filing, repatriation) | −1,200 | 2.9% | Provider |

| Vacancy buffer | −1,800 | 4.3% | No |

| Net to owner | 19,500 | 46.4% | 5.9% net |

Two real levers. Operator share has elasticity in the 25‑35% band depending on inventory size and contract length. Provider choice on the admin line can save USD 400‑600 a year. The rest of the stack is what it is.

Marketing materials are written in gross terms during ramp-up year, in peak season, against a guarantee that lapses by year three. The honest comparison runs against the rolling five-year mean. Below is what each operating mode actually delivered across the MORE Group cohort, side-by-side with how it was originally pitched.

| Operating mode | Pitched | Y1‑3 | Y3‑5 | Why the gap |

|---|---|---|---|---|

| Long-let | 7‑8% | 5.0‑6.0% | 5.5‑6.5% | Turn, fee, void. |

| Hotel-managed | 8‑10% | 4.5‑6.0% | 6.0‑7.5% | Operator share, FF&E. |

| Self-run | 10‑12% | 5.5‑7.5% | 6.5‑9.0% | Cleaning, channel, void. |

| Hybrid | 9‑11% | 5.0‑6.5% | 6.0‑7.5% | Cost without scale. |

One. A guaranteed yield above 7% net for more than three years means the buyer holds the credit risk — usually priced into the asking price.

Two. Self-run beats hotel-managed only for on-island owners treating it as a part-time business.

Three. Reliable matches cluster around 5.5‑7.0% net. Higher numbers come with attached risks.

Every foreign-owned residence on Phuket is run on one of three programmes, or a managed hybrid of two. The structural differences sit in the contract; the experience difference sits in who picks up the phone when something breaks at 11pm.

| Programme | Operator | Vacancy carried by | Owner share | Owner-use |

|---|---|---|---|---|

| Pool | Developer in-house, often white-labelled. | Pooled, by m². | 60‑70% | 14‑30 |

| Hotel-managed | International operator, full hotel SOPs. | Operator marketing; owner unit void. | 55‑70% | 14‑28 |

| Self-run | Owner + cleaning, channel, agency. | Owner, every night. | 75‑90% | ∞ |

The decision is driven by three buyer-side variables, in this order: distance from the asset, tolerance for variance, desire to use the property personally. A London buyer who visits twice a year picks the pool programme every time. An on-island owner with contractor relationships will out-yield the pool by 150‑200bps running it themselves — paying for the privilege in time.

A note on guarantees. Year one and two yield guarantees are typically funded by a 3‑6% uplift in the asking price. Buyers pay for their own guarantee.

Headline yield is what the developer prints. The clauses below are what you actually own — or, more accurately, what the contract owns of you. Each has appeared often enough in our intake reviews that we now flag them automatically.

| # | Clause | Standard market | Negotiate to |

|---|---|---|---|

| 1 | Revenue share | Operator 35‑40%, owner 60‑65%. | Operator 25‑30% on inventory >40 keys. |

| 2 | FF&E reserve | 3‑5% of gross, owner-funded. | Cap at 3%; itemised 5-yr plan. |

| 3 | Owner-use nights | 14 nts, peak excluded. | 21‑30 nts; 2 peak weeks on 6-mo notice. |

| 4 | Exit penalty | 6‑12 mo operator fees on early exit. | Sliding scale: 100% Y1, 50% Y2, 0% Y3+. |

| 5 | Yield guarantee | 5‑7% for 1‑2 yr; opaque mechanics. | Remove (price cut) or extend with audit rights. |

| 6 | Reporting cadence | Quarterly, no audit rights. | Monthly; annual audit at owner cost. |

| 7 | Renovation pass-through | Operator decides; owner pays share. | Owner consent >USD 5K; block on luxury. |

| 8 | Termination by owner | Operator’s discretion; rarely contractual. | 6-mo notice, no penalty Y3+, FF&E preserved. |

Where the leverage is. Inventory size and exclusivity. Pre-launch, the developer moves on two or three lines. After completion, none.

Same one-bed in Bang Tao, gross USD 42K. Three programmes, three cash-flow waterfalls. The number that matters is the bottom row; the lesson is the row that produced it.

| Cash-flow line | Pool | Hotel | Self-run |

|---|---|---|---|

| Gross rental | 42,000 | 45,000 | 38,000 |

| Operator / agency fee | −13,000 | −15,000 | −5,000 |

| Channel & OTA commissions | included | included | −4,500 |

| Cleaning, linen, consumables | included | included | −3,800 |

| FF&E reserve | −1,500 | −1,800 | −1,200 |

| CAM, sinking, master-insurance | −2,800 | −3,200 | −2,800 |

| Local property tax | −500 | −500 | −500 |

| Withholding on rental | −2,100 | −2,400 | −1,900 |

| Owner admin / repatriation | −1,200 | −1,200 | −1,800 |

| Net to owner | 20,900 | 20,900 | 16,500 |

| Net yield (on USD 500K) | 4.2% | 4.2% | 3.3% |

| Owner time per year | ~2 hr | ~3 hr | 80‑120 hr |